How Bank Reconciliation Works and Why It Is Important

- July 29, 2020

- admin@ohi

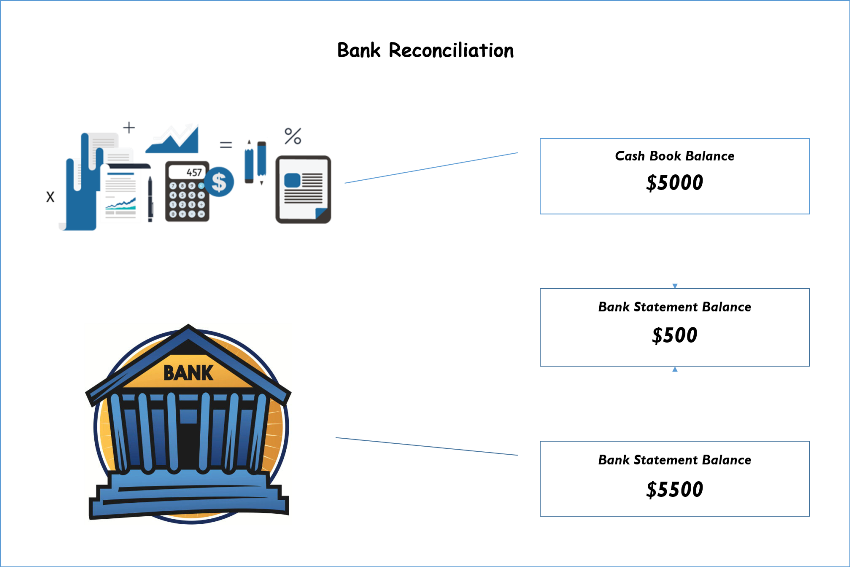

Reconciliation of your business bank account implies that you are comparing your internal financial records against the records supplied to you by your bank.

A monthly bank reconciliation enables you to identify any suspicious transactions that could potentially be fraud or accounting errors, and the practice also helps you identify inefficiencies.

To reconcile your bank accounts, compare your internal record of transactions as-well-as balances to your monthly bank statement.

Corroborate every transaction meticulously, ensuring that the amounts match perfectly, and spot any differences that need further investigation.

You also need to make sure that your bank statements display ending account balance that complies with your internal records. If the amounts mismatch, you are liable to receive an explanation for the glitch.

The role of bank reconciliation process demands the following –

The entire model of operation can be as formal or informal as you’d prefer. Some businesses produce a bank reconciliation statement to document their regular reconciliation of accounts.

If you cannot complete the process monthly, you can choose to perform it daily, quarterly, or for any other interval as per your convenience.

Your accounting system must contain all of the internal transaction data you require, else you could choose to keep your records in a check register, which could be electronic or on paper.

Your bank can render online access to your account, enabling you to view and download transactions regularly for a detailed juxtaposition.

Some online accounting programs choose to partially automate the process, but you still are required to supervise the process.

If balancing your check book is something that you’re familiar with, then you’re already familiar with bank reconciliation. It’s primarily performing the same thing for the same reasons.

It’s perfectly normal to witness minor differences that have surfaced due to timing, which might include items that haven’t yet been cleared by the bank, but you should be able to justify those differences with ease.

For instance – You might write a check to a vendor and lower your account balance on internal systems as per your convenience, but your bank continues to display a higher balance until the check is deducted from your account.

Such checks are termed as outstanding checks.

An automatic electronic payment could clear your account a day prior or after the end of the month, and you could have anticipated seeing that change in a different month.

When you can conveniently account for discrepancies, there exists no reason to worry. If it takes greater time to identify and reconcile discrepancies, there might be bigger issues that need to be addressed.

A regular review of your accounts can help you identify problems way before they slip out of control.

Business bank accounts are entitled to less protection than consumer accounts under federal law, making it is especially vital for businesses to eliminate problems quickly.

You can’t always count on the bank to cover fraud or errors happening in your account.

Being wary of initial signs of fraud must be your priority while reconciling transactions in your bank account.

There are a few things that you need to consider namely –

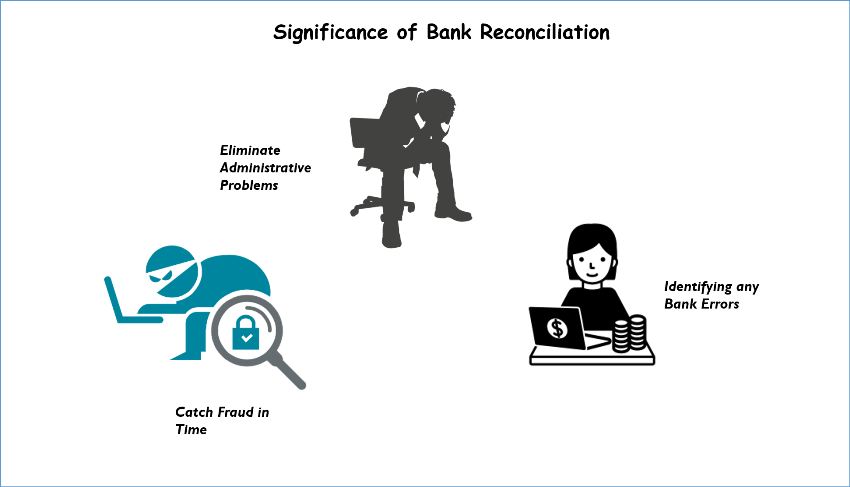

Reconciling your account can help you spot internal administrative issues that need proper addressing.

For instance, you might need to recalculate how you deal with cash flow and accounts receivable, or maybe change the record-keeping system or the accounting processes used by you.

Proper processes to manage your banking transactions result in outcomes such as:

To understand how to effectively manage your bank accounts as your business expands, consider speaking with the treasury management department at your bank or credit union.

It’s advisable to review your bank accounts at least once a month.

For high-volume businesses or scenarios with a higher risk of fraud, it would be best to reconcile your bank transactions more often than just monthly. Some companies reconcile their bank accounts every day.

You can also add protection into your bank accounts, and your bank can input some useful ideas.

For instance, many banks offer a solution termed as Positive Pay, which prevents your bank from validating payments out of your account until you provide instructions to warrant individual payments in advance.

Bank reconciliation is paramount as it keeps your accounts safe and helps you check for any suspicious activities that might otherwise go unnoticed.

Your bank can provide you with various security options to choose from to safeguard your account from fraud and errors.

A bank reconciliation process can also help you keep updated with the latest transactions and any outstanding amount that needs to be paid to customers or towards credit bills. In case a mishappening or fraud occurs with your bank account because you did not reconcile your accounts timely, you cannot necessarily approach the bank to claim your lost funds.

Thus, it is advisable to keep errors and fraud at bay by reconciling your accounts after specified intervals.

OHI is a specialized finance and accounting outsourcing service provider with over fifteen years of finance and accounting outsourcing experience. We have strong functional outsourcing expertise in end to end accounting processes covering daily accounting activities, reconciliations, month end and year-end account finalization processes, employee reimbursements, payroll processing, management reporting and financial analysis.

OHI serves close to 300+ clients across USA, UK and Canada. We invite you to experience finance and accounting outsourcing through us.

Learn More About Our Accounting Services including Reconciliations: Call us at 1-646-367-8976, Email at sales@outsourcinghubindia.com – CONTACT US

Contact us for a customized NO OBLIGATION proposal for outsourcing your accounting activities.